Good morning, so Apple http://www.marketwatch.com/investing/stock/aapl & Twitter http://www.marketwatch.com/investing/Stock/TWTR?countrycode=US disappointed with earnings & down -9% & -13% in after markets trading. With AAPL one of the most widely held stocks by hedge funds, the pain continues for whole sector. Only Goldman & Morgan Stanley relatively still upbeat on oil with GS analyst on CNBC propping it http://www.cnbc.com/2016/04/26/big-oil-may-have-to-cut-dividends-goldmans-jeff-currie.html saw S&P500 & Dow supported ahead of FOMC decision early tomorrow Asia morning. GBP squeeze rally continued with spike to 1.4635 as Brexit odds reduced by London bookmakers. 1.47/1.48 is not unthinkable as poor crowded GBP brexit shorts look to exit as odds reduce further http://www.bloomberg.com/graphics/2016-brexit-watch/ … GBP/AUD cross does seem to bottom at 1.84 last Friday & a medium rally to 1.97-2.01 seems plausible noting that GBP/AUD has almost 90% correlation to VIX & general risk off … is this an early leading indicator?

World Cup 2014 … Asian telcos & cable operators … between a Rock & a Hard Place

Asian telecommunication companies (telcos) have long enjoyed oligopolistic hold in their respective markets in the past 2 decades when Asians found their love with mobile phones, internet broadband & cable TV. From the normalised (adjusted to USD) chart above (encompassing Singapore, Malaysia & Hong Kong telcos & cable operators), since the 2008 financial crisis, they have managed to performed very well indeed given their phenomenally stable earnings & relatively high dividend yields averaging 2.5 – 5% in general.

However, all good things must come to an end, sometimes it is some disruptive technological change or advance that renders certain businesses and processes obsolete. We have seen that with the steam locomotive, polaroid instant snaps, Xerox copiers, pagers, … the list goes on. The roll-out of 3G-4G networks and fast breakneck fibre broadbands across Asia encouraged the growth of social media, peer-to-peer streaming & other usage of applications that are able to harness the tremendous speed & connectivity into the last mile into Asian consumers’ homes & even when they are on the move. However, the country / domicile walls that these oligopolistic Asian telcos & cable operators have enacted in the past with their respective government support are crumbling down fast!

The key is that there are serious dearth of unique domestic content & services provided by all these Asian telcos & cable operators. Most contents, apps and media come from the West or recently from China, Korea & Japan that all the Asian operators syndicated, bought or licensed from. This extends to the current FIFA 2014 World Cup that has enthralled all viewers around the world. The ridiculous price that Singapore football fans have to endure to watch the World Cup matches http://www.goal.com/en-sg/news/3880/singapore/2014/03/18/4690244/singapore-costliest-place-to-watch-world-cup is a case study of what has gone wrong in ”paying based on where you happen to live” when it can be free or much cheaper even within other Asian countries.

Asianmacro has been using a VPN service so that he can simply be in the USA, UK, Europe, Latin America or any other country he fancies as identified by his IP address & gateway / DNS to provide security for his online activities. The fringe benefit to this is I have access to watch all the FIFA 2014 World Cup matches for free in those countries that provide free viewing to residents in them too (where Asianmacro will be simply be there by choosing to be there online)!

I have taken profit on my long position in Asian telcos like Singtel recently. While I am not going short these stocks as they pay relatively high dividends that many yield hungry investors do chase, the question that we should be asking is whether Asian telcos really have a future besides being “dumb pipe” gateway providers in communications & media, without any real innovative apps or unique domestic content that people want & will pay for!

P.S. And asking Whatsapp or Skype to pay for using its network by Singtel’s CEO is definitely not the way to go! http://www.techgoondu.com/2014/02/26/commentary-singtel-wants-whatsapp-and-skype-to-pay/#.U6wq8PmSySo

Call me a lunatic … calling a short term market top

Asianmacro had previously called for a continuous rally in S&P500 when it was at 1880 around May 24 and it has advanced almost 4% since https://asianmacro.com/2014/05/24/path-of-least-resistance-is-up/. Back in May, many doomsayers were on CNBC and various media calling for an impending collapse of even 10-15% in stocks. But looks like the shorts and underweights in equities and bonds were all forced to scramble and had to catch up with their benchmarks that they are underperforming against.

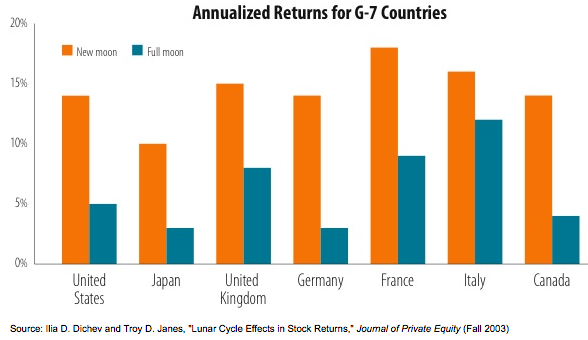

However with the impending Full Moon on June 13 and the onset of the FIFA2014 World Cup, I am now calling for caution. Generally, stocks tend to perform better in the days around the New Moon, while price weakness is often seen in the days around Full Moon as seen in the chart above. Many research have touched upon this topic like this here http://papers.ssrn.com/sol3/papers.cfm?abstract_id=281665 and an example of lunar-cycle trading by other traders can be found here http://lunatictrader.com/?Moon_Cycles:Lunar_Phases and http://www.ftsefreedom.com/2012/08/how-moon-affects-trader-sentiment-and.html.

However, another indicator which is the USA Federal Reserve Money Supply M2 yoy growth that I track to give me an idea of the pace of liquidity creation in the US monetary system. It has peaked in 2012 in spite of further QE which has propelled the equity markets higher. M2 in itself don’t mean much but belongs to an array of economic & other market indicators which I track. While we might see S&P500 ending higher and maybe even cross 2,000 level by December 2014. But Asianmacro will take his chips off the table for now, pour himself a glass of nice burgundy, followed by a fabulous single malt whisky and watch the FIFA2014 World Cup action unfold. The market is now left to the losers who need to be around. Not me!

Waiting with bated breath for Thursday ECB meeting

Asianmacro has many close friends in the ”real world” i.e. people who are engaged in real productive businesses or employment like doctors, engineers, businessmen, lawyers (OK maybe not lawyers) …. where FOMC. ECB, QE & other financial lingo don’t mean much to them! However, what you do not know nor care in your regular life in going for work in the morning at 9 a.m., punching out at 5 p.m. (if there is even regular hours anymore like days of old!) does not mean that you will not be affected by events & developments which only financial market practitioners care about to monitor with a hawk eye.

In fact since the 2008 global financial crisis, everything that has happened especially in the real world & economy affecting many lives can be traced back to financial markets development & actions taken by governments & central banks since.

The most important event coming up with reverberating effects globally with be this upcoming European Central Bank (ECB) meeting on Thursday 5 May. All expectations are on Draghi, the ECB President to cut Eurozone refinance rate and unleash their version of QE as well. http://www.reuters.com/article/2014/06/02/us-markets-forex-idUSKBN0EA11M20140602 . From the chart above, we can see that EUR/USD has plunged from 1.40 to 1.36 currently in the past one over week end May as short positions (*best captured by the IMM CFTC net non-commercial positions) reached the highest level of shorts in 2014. Risk reversals volatility prices (where price of calls over puts) have fallen as well with options market pricing more demand for EUR puts over calls.

In the chart below, in fact, Citigroup Pain Index is at an extreme negative level. This is a FX Positioning Alert Indicator that infer positioning of active currency traders from relationships between exchange rates and currency managers’ returns. A positive reading suggests that currency traders have been net long the currency and a negative reading suggests that currency traders have been net short the currency, and in this case, the market is extremely short EUR.

We can also see that the yield spread between 2-year EUR rates & USD rates have gone to an extreme level since EUR rates fell a lot more & quicker in the recent weeks vis-a-vis USD rates.

When the entire sell-side screams for lower EUR & for further short EUR recommendations into ECB meeting, this is when Asianmacro gets worried over the imbalance of sentiments. Sometimes, the markets have no logic beyond street positioning & will go to the maximum pain to squeeze out the weak hands. As such, I have close out my short EUR/USD position & in fact turned long via 3-day EUR 1.3600 strike call options NY cut expiry (NYC 10 a.m. expiry which is right after ECB meeting decision & when the ECB press conference is underway). From illustration below, it cost my only 33 b.p. (or an equivalent of 40 pips in FX terms) with breakeven at 1.3640. If Draghi underwhelms in delivering an ECB cut & tone in his press conference, EUR/USD might just fly up to 1.3750-1.3800 level and I will be a happy man via my options & allow me to re-sell EUR/USD to take profit & establish new EUR shorts if it make sense again. If ECB overwhelms with aggressive cut & dovish undertones & EUR/USD plunge further, I don’t lose much beyond my small option premium for the call option that will expire worthless.

Path of least resistance is … UP!

There have been many naysayers & dooms -day-prophets in the markets lately. It’s always easy to call for a 10-20% correction in stocks & general markets & saying ‘Sell in May & go away!”. The key is when precisely? And also after all the selling in protecting your downside if you cannot take the temporary marked-to-market pain; when & how are you going to get back onto the financial market bus before it speeds off again without you is key!

Sometimes when everybody call for a market correction or move in either direction up or down, usually, it just ain’t gonna happen that way. Just like the past week when calls of 1815 or 1780 in S&P500, a 5% correction to the downside seems imminent … we end up at almost 1900 by the end of the week.

Asianmacro likes to look at relative performance of EEM vs SPY (the Emerging Market ETF vs S&P500 ETF) as an indicator of flow of funds between developed & emerging markets whenever the direction of the general market is uncertain. From the chart above, we see that SPY has outperformed EEM since 2010 till January 2014 when it reversed. The biggest components of EEM are the likes of Samsung Electronics (3.93%), Taiwan Semiconductor (2.50%), Tencent (1.88%), China Mobile (1.55%), China Construction Bank (1.31%); where the top 5 names account for about 11% weighting & all are from North Asia.

From the chart below, new units creation in EEM have been driving the rally outperformance of EEM evidently. The question now is will we see this continue or we might have plateaued & reverse instead?

It does seem that in the short run, perhaps we just might especially if China is relaxing the foreign investment rules http://online.wsj.com/news/articles/SB10001424052702303749904579579670989773760?mg=reno64-wsj&url=http%3A%2F%2Fonline.wsj.com%2Farticle%2FSB10001424052702303749904579579670989773760.html. In addition, EUR/AUD FX cross continues to head lower with VIX and all signs do point to S&P500 crossing & powering higher above 1900 despite the howls of protests by the bears that was touched upon in my previous post on a summer melt-up rally in risky assets https://asianmacro.com/2014/05/13/the-summer-carry-melt-up-in-risk-assets/.

Remember, the path of least resistance is … UP … as this is when it’s most painful for everybody who’s gotten off the financial market bus & have not got back in again!

Full moon reversal & doing nothing .. football might save the world

It was a full moon last night on 14 May 2014 & usually more often than not, it signals a short term market top or reversal especially in equities. We did see an intraday high where S&P500 pushed above 1900 before reversing lower. It does not mean that we do not get a potential summer rally squeeze in risky assets https://asianmacro.com/2014/05/13/the-summer-carry-melt-up-in-risk-assets/ as we are not into summer yet but just knocking the door around the corner.

However, it does bring to mind the uncertainty & sense of not knowing what to do on certain days with conviction especially by the humble Asianmacro here who is only a small minion in the big scheme of things in the financial markets. The only thing that made sense is the video clip produced by Samsung assembling some of the best footballers on Earth to save us from an Alien invasion where the outcome is determined by a football match .. what else is new!

From the chart above, if you look at the spread between the 1st & 2nd VIX futures contract, we are back again to 155 b.p. difference. Usually a big & growing difference where the 2nd contract value is greater than the 1st contract value implies an upward sloping volatility curve (for VIX) & represent a normalisation of sentiment (or complacency). A small or narrowing difference and in the extreme when it goes to negative value implies an inverted volatility curve (for VIX) where heightened fear of imminent risk of crash in markets resulted in buying of volatility (or VIX) in near contract over that of far contracts.

The above is just a generalisation so as not to bore most of you who might not be equity derivatives & volatility traders. However, as you can see above, whenever we reach 155-175 b.p. spread in VIX 1st & 2nd futures, we do see a correction lower in S&P500 subsequently for a short period of time. Anyway, there are just so many mixed signals in the markets at the moment. Sometimes it’s best to just sit back on the sidelines & wait …

“The desire for constant action irrespective of underlying conditions is responsible for many losses on Wall Street even among the professionals, who feel that they must take home some money every day, as though they were working for regular wages.” – Jesse Livermore

FIFA14 World Cup and financial markets

Football, rugby, cricket, baseball, (*OK American football & Aussie rules football too just to be inclusive) are popular sports with most in the global financial markets. With the impending FIFA14 World Cup upon us in summer, what will happen to the traders & portfolio managers in banks, hedge funds, pension funds, mutual funds & insurance companies? Short of abandoning their posts, their attention will be on the TV in the dealing room playing that match while they root for their teams. Only the algos running the HFTs machines will continue to do their work unfailingly!

There have been many research done in the recent past to suggest anaemic volumes in stock markets & also of declines when a country loses a game http://www.nltimes.nl/2014/01/29/world-cup-losses-trigger-stock-market-drop/. Even the venerable ECB had done a study on it before http://espn.go.com/sports/soccer/story/_/id/7573861/stock-market-trading-slows-world-cup-study-says as reported & the actual study can be seen here http://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp1424.pdf.

However, this FIFA14 World Cup fever does increases the likelihood of the potential path of least resistance .. which is for a higher stock market & in risky assets in general as uninvolved cash on the sidelines, cautious traders & portfolio managers failed to invest & tracked the grinding higher markets. Perhaps, the silent algos in HFTs who do not watch any FIFA14 World Cup matches might get it right & actually be the culprits pushing & buying the markets even higher from here!

The summer carry melt-up in risk assets

The hardest trade to put on mentally & physically in execution more often than not ends up being the right profitable trade. This was learnt the hard way by Asianmacro over the years like when overnight & tomorrow/next Thai-baht (THB) rate was at 10% at mid-day at the onset on the Asian crisis in May 1997, when it was only 3% in the morning, it still made sense to pay up to secure any funding if you really need them. It ended up at 1,000% by late afternoon & everything keeled over.

There is a sense of deja-vu at the moment except that this time instead of the markets keeling over, there seems to be a slow motion melt-up in risk assets led by U.S. stock markets with S&P500 leading the way while Nasdaq100 & Russell2000 recovered from their respective corrections over the recent weeks.

From the chart above, where both the EUR/AUD FX cross & VIX bear high correlation & R-square with each other. Everything seems to suggest with declining VIX and a continued search for FX carry best represented by EUR/AUD shorts (to earn the interest rate differential between EUR & AUD) … the pain trade is to see risky assets melt up even more into summer!

To Kill a Mocking Treasury note

It has been tough trading & positioning in interest rates in 2014. Anybody telling you otherwise is either lying or very lucky. From the chart above, you can see that U.S. 10-year Treasury note yields have moved from 3.10% to 2.55% in January; and ever since whipped around every 1 – 2 weeks between 2.55% & 2.80% very erratically … Mocking at all bulls & bears in Treasuries.

Now every lay person will say that it then presents a simple ”range trading” strategy of 2.55 – 2.80% for the supposed smart trader to monetise. Well in real life, it might not be so simple as the prices gap back & forth and the supposed extremities occur during U.S. economic data releases in very short time frames in a blink of an eye more often than not. As such, you will be lucky to capture at most 50% of these moves. And if you are unlucky, you get stopped out at some of these ”instant algo flash up or crash down” while still building your positions. And we are talking about ”basis points” here … where making 10 b.p. or 0.10% is like a home run these days! Something that any lay person on the street will not really care about or bother.

During such times, perhaps it is the ”no stops”, ”no leverage” & ”no haste” real money investing approach that works best in the bond markets now. Essentially replicating a ”long gamma” approach of ”buying low” and ”selling high” … in putting on positions at the 2.55 – 2.80% range with preparations for overshoots at times but not stopping out.

Asianmacro is short June14 10-years Treasury futures late last week (i.e. paid rates & betting on higher yields in the interim).

How many screens do you need?

This dude beats me hands down. Mrs Asianmacro thought my 12 screens set-up was already an overkill, wait till I show her this!

Once upon a time, except for the CEO of the investment bank who does not even need a PC as everything is screened & read out to him by his assistants. The sign of how important a trader was lies in the number of screens & where he/she sat in the dealing room. Only the BSD (*whether he has a screen each to play youtube, PC games instead of actual price/data stream does not matter) sat in prime real estate right in the middle of the dealing room with the minions spread out into the ‘suburbs’ with their miserable 2 – 4 screens standard set-up. Anyway supposed trading heads in banks or hedge fund honcho with only 1 – 2 screens have either gone managerial full-time or achieved nirvana like Warren Buffet where he just buys and hold forever.

Over the years, through trial & error, Asianmacro has found that 8 – 12 screens work best as everything will be within peripheral eye-ball view of about 140 degrees. Anything more becomes bragging rights … anything less, you probably need many minions to monitor & execute on your behalf.